Do Security Tokens Need a New Blockchain? Benefits and Challenges [Part I]

By Laura Desmond

This week at the Crypto Invest Summit, Spice VC’s partner Ami Ben-Davidunveiled his vision for Ownera, a new blockchain for security tokens. Ami was kind enough to brief me on his ideas for Ownera months ago and I’ve been thinking about the subject ever since. The concept of a new blockchain for crypto-securities is far from trivial and certainly a sensitive topic in the crypto-securities community. To try to explore this subject in detail, I’ve divided this essay into three main parts to present both the benefits and challenges of this new angle in the security token market.

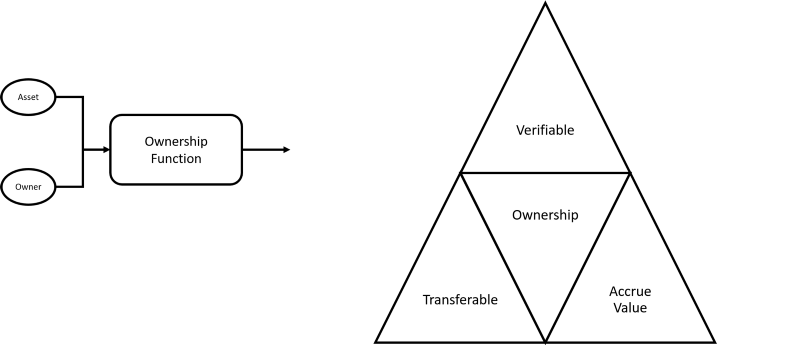

If we stripped down all the technical complexities, the idea of a blockchain for security tokens boils down to a very simple question: can we represent ownership effectively by simply using smart contracts? Mathematically, ownership can be represented as a relationship between an identity(owner) and an asset. Conceptually, ownership has to have some basic properties: it has to be verifiable, transferable and accrue value based on market dynamics.

Ownership is the main principle of security tokens. At the moment, we are hacking our way trying to model ownership dynamics on top of blockchain runtimes that were designed for asset transfers. The question is whether ownership deserves to be a tier1-citizen in a blockchain.

Proof by Contradiction

An interesting way to determine whether security tokens deserve their own blockchain is by trying to validate the opposite assertion. Proof by contradiction is a mathematical technique that tries to prove an assertion by disproving the opposite proposition. In that sense, let’s assume that we believe all security tokens will be built in a blockchain runtime like Ethereum and try to disprove that assertion.

Any blockchain runtime can be decomposed as a technological layer, incentive mechanism and a node architecture. The technological layer is responsible for aspects like block issuance, transaction recording etc. The incentive mechanisms abstract areas like consensus, token minting and several others. Finally, the node architecture describes what type of roles different nodes play in the network. Blockchains like Ethereum were fundamentally designed for asset transfers and, therefore, have built the technological building blocks, node architecture and incentive mechanisms to support that model.

Building security tokens on top of Ethereum essentially means that we will adapt those mechanisms to support ownership dynamics. While the technological building blocks of a blockchain can work consistently for asset transfers and ownerships, I don’t think we can claim the same for the node architecture and incentive mechanisms. Thinking that the same miner that validates an Ethereum transaction is equipped to do a capital-requirements validation on a specific node is a bit of a stretch. Similarly, thinking that the incentives for mining an Ethereum transaction are the same as validating the transfer of a real estate token between two parties seems like a poor generalization.

If the previous points were not enough to convince you about the challenges of relying of Ethereum for security tokens, we also have the subject of identity. Security token transactions rely on identity as a first-class building block. However, runtimes like Ethereum are designed for pseudonymity and introducing identity violates some of its core principles. How is that for a contradiction?

The Risk: Recentralizing the Blockchain

The challenges listed in the previous section makes it extremely difficult to adapt blockchains like Ethereum to the world of security tokens. If that’s the case, how are companies issuing security tokens today? Very simple, by introducing centralized components into the security token architecture. I like to call those components re-centralization vectors.

The current generation of security token platforms operate as centralized entities on a decentralized runtime by introducing recentralization vectors such as compliance validators (KYC/AML), off-chain processing etc. Those type of shortcuts are necessary not only to overcome the technical limitations of Ethereum but to simplify the issuance of security tokens in a very immature market. However, if we introduce too many recentralization vectors we might end up neglecting the value proposition of the blockchain in the first place. If we take that vision to an extreme, we might not need a blockchain for security tokens at all.

The Emergence of Specialized Blockchains

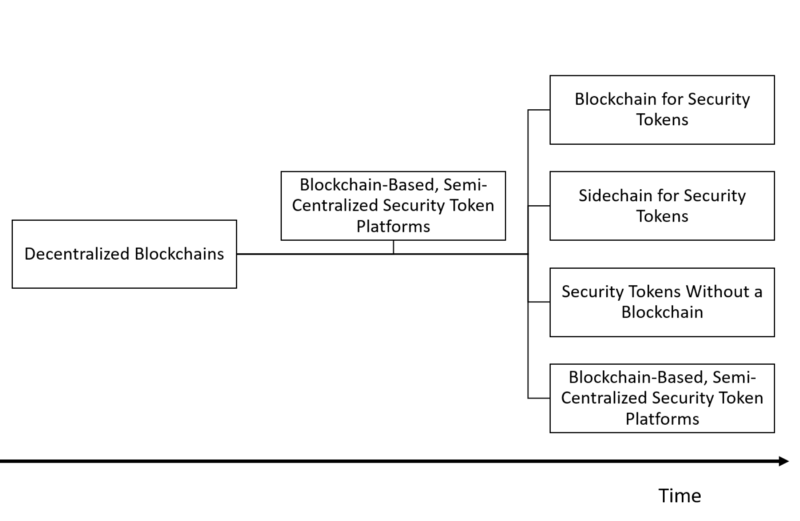

The blockchain ecosystem is evolving as a combination of general-purpose and specialized blockchains. EOS, Ethereum, Hyperledger fall in the camp of general-purpose blockchain that enable the implementation of almost-any decentralized use case. Blockchain like Stellar, Ripple or IOTA focused on solving specialized use cases like payments or device interactions. The second group of blockchains emerge because the incentives of the use case were strong enough to justify a new runtime. If you believe that premise, then we need to ask ourselves whether security tokens deserve their own blockchain.

In the second part of this article, I am planning to explore the technological building blocks of a potential blockchain for security tokens.